There’s a reason the same names keep showing up in every “greatest wealth creators of the past 20 years” list.

Apple. Amazon. Google. Microsoft. Nvidia.

Different industries. Different founders. Different decades of dominance. But one shared trait that most investors overlook entirely: they didn’t just win their markets. They made it structurally impossible for anyone else to win them.

That’s not a coincidence. It’s a pattern — one that stretches back eighty years of market history, and one that a new ETF has finally turned into a systematic investment strategy.

The Insight Hidden in a Board Game

Most investors learn about diversification, P/E ratios, and dividend yields. Very few are taught the most important lesson hiding in plain sight inside a game most of us played as children.

In Monopoly, the player who buys a little of everything — spreading properties across the board — almost always loses. The winner is the player who locks down a color set, builds houses fast, and turns every opponent’s move into a rent payment. It’s not about how many properties you own. It’s about making a portion of the board inescapable.

The same dynamic has quietly governed the stock market for decades.

“Every market legend — from Apple’s iPhone ecosystem to Google’s search engine and Amazon’s logistics network — figured out how to corner a space,” says Neil Azous, portfolio manager of the Monopoly ETF (ticker: MPLY). “They built pricing power, loyalty, and data advantages that compound over time.”

The companies that have generated the most long-term wealth for investors share a specific set of traits: control of distribution, data, or user ecosystems. Not just good products. Not just strong management. Control. And the data on what that control is worth is striking.

What Eight Decades of Market History Actually Shows

Strategy Shares’ research team spent years dissecting the long-term performance of stocks across industries and market cycles, going back to the 1940s. The question they set out to answer wasn’t “what makes a stock go up?” It was more specific: what separates the stocks that compound wealth for 20+ years from those that don’t?

The answer came back consistently: market concentration.

Companies that held over 50% market share in their core segment — what Azous calls an “economic monopoly” — generated average annualized returns nearly twice that of the S&P 500 over a 20-year horizon. They also maintained fatter gross margins, lower customer churn, and superior pricing power through recessions, rate cycles, and competitive disruptions that wiped out their rivals.

The logic is straightforward once you see it. When a company achieves structural dominance — when switching away from it becomes painful, when its network gets stronger with every new user, when its data advantage is simply too large to replicate — earnings don’t just grow. They compound with a consistency that blunt valuation metrics like P/E ratios simply can’t capture.

“Wall Street still thinks in linear terms — revenue, margins, growth,” Azous says. “But the new economy compounds through monopolistic feedback loops. Once a company hits critical mass, it’s game over for everyone else.”

Why Your Index Fund Isn’t Enough

Here’s the objection every smart investor will raise: Don’t I already own Apple, Microsoft, and Google through the S&P 500?

Yes — and no.

A standard S&P 500 index fund owns all 500 constituents, weighting them by market cap. You do get exposure to dominant companies. But you also get equal structural exposure to hundreds of businesses with no moat, no pricing power, and no defensible position — companies that will spend the next decade fighting for margin against well-resourced competitors.

MPLY is built on a different premise: not all exposure to great companies is equal. The Monopoly ETF doesn’t just own names that have historically dominated — it weights them according to how deeply and durably that dominance is currently entrenched, using a proprietary Dominance Scoring System that evaluates each holding across five measurable dimensions:

· Market Control — the degree of ecosystem dependency competitors and customers have built around the company

· Network Effects — how each new user or transaction strengthens the moat

· Pricing Power — demonstrated ability to raise prices without demand destruction

· Switching Costs — the measurable friction a customer faces when attempting to leave

· Reinvestment Edge — how efficiently the company channels its dominant cash flow back into widening the moat

Each company receives a composite Monopoly Score. The portfolio tilts heavily toward those at the top — firms like Microsoft, Visa, Meta, Broadcom, and Amazon — not just because they’re large, but because their score reflects structural inevitability, not recent momentum.

Think about what that distinction means in practice. Nvidia doesn’t just sell chips. Its CUDA software framework has made an entire generation of AI developers fluent in Nvidia’s proprietary language. Switching to a competitor’s hardware means retraining teams, rewriting codebases, and absorbing years of lost productivity. That’s not a product advantage. That’s a Boardwalk-with-hotels advantage.

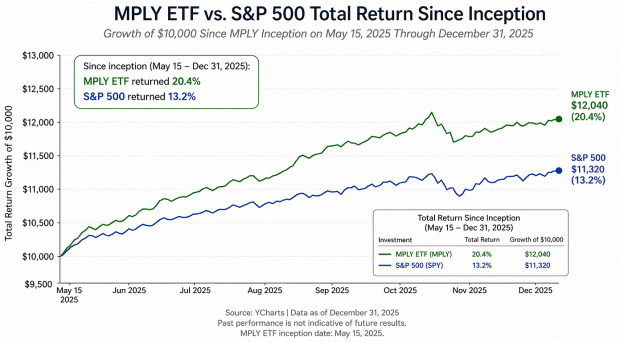

Since its launch in May 2025, MPLY has returned 20.4% through year-end, compared to 13.2% for the S&P 500 — outperforming the benchmark by more than seven percentage points in under eight months.

Early performance in any new fund deserves scrutiny, and intellectually honest investors are right to apply it. Seven months is not a definitive track record. What it is — in a period that included significant macro volatility — is an early-stage proof of concept for a thesis that eight decades of underlying market data already supports.

There’s also a more important point: you’re reading about this fund early. The structural advantage strategies that seem obvious in hindsight — buying Amazon in 2005, holding Google through 2010 — were available to investors who recognized the dominance dynamic before it was consensus. MPLY is an attempt to systematize exactly that recognition.

“History tells us monopolies evolve,” says Azous. “Twenty years ago, nobody thought digital payments or cloud software would become trillion-dollar moats. Our goal is to identify those dynamics early — the companies quietly cornering a market before the crowd notices.”

The fund’s research team is already scanning mid-cap and frontier names in AI infrastructure, cybersecurity, and digital health — sectors where the next generation of economic monopolies is currently being built. Positions in these emerging moats are being sized now, before the hotels go up.

A Surprisingly Diverse Portfolio, Unified by One Idea

Despite its concentrated philosophy, MPLY’s holdings span sectors in a way that surprises first-time observers. Technology anchors the portfolio, but the fund also holds dominant positions in consumer platforms, financial infrastructure, healthcare, and industrial software.

Consider Eli Lilly. Its early commanding position in the GLP-1 obesity drug market represents the same moat dynamic as any platform company: first-mover scale, manufacturing capacity that took years to build, clinical data advantages that reinforce physician loyalty, and a brand association with an entirely new category of medicine. That’s pricing power. That’s switching cost. That’s a Dominance Score.

The common thread isn’t sector. It’s control of the profit pool. Whether a company controls digital search, payment rails, enterprise cloud infrastructure, or a novel drug class, the compounding economics follow the same logic.

The Investor’s Choice

Every investor faces the same fundamental question: are you trying to guess which unpredictable events will move which stocks next quarter? Or are you trying to own the structural winners of the next decade?

The first approach requires being right about things that are inherently unknowable. The second requires recognizing something that history has confirmed repeatedly: the companies that control their markets don’t need luck. They need time.

In Monopoly, you can spend the whole game chasing every roll of the dice — scrambling for properties, hoping for lucky draws, reacting to everyone else’s moves. Or you can recognize the board early, buy the right positions, and let everyone else pay you rent.

MPLY is built for investors who understand which strategy actually wins the game.